Global Mobility and the Tax Question

With the wave of tax, property and superannuation changes proposed and incoming in Australia, some entrepreneurs and wealthy are considering relocating to other more favourable tax jurisdictions.

I believe this is not simply to avoid tax, but reducing it to a level that continues to stimulate innovation and entrepreneurship, whilst seeking other economic factors aligned with values. The current government is effectively applying a wage-earner framework to all Australians, and the longer term consequence of this will be to stifle the very people who create jobs, build businesses and keep Australia competitive globally, especially at a time of such profound technological disruption.

Some argue Australia is the best country in which to live and I don't disagree. We have a stable economy, a democratic government, an excellent standard of living and of course the lifestyle! But moving countries is easier said than done. I have done it twice, the second time with young children, and it is an absolute mission. For most people, it stays firmly in the "too hard" basket. For the ultra wealthy and/or entrepreneurial, however, it is entirely a possibility, and one that is becoming increasingly attractive as these policy settings tighten.

And so, I offer below some insights on global mobility. Firstly a case study with Peter Thiel, billionaire tech entrepreneur and venture capitalist, moving to Argentina and secondly an analysis of some of the most prominent tax jurisdictions in the world and the realities of moving there.

Part One: The Peter Thiel Case Study

When Peter Thiel announced plans to relocate to Argentina, the financial press did what it always does and reached straight for the tax explanation. It is true that California, where Thiel built much of his fortune, has proposed a 5% annual wealth tax on its highest net worth residents, an extraordinary impost that would apply to global assets regardless of where income is earned. A push factor, certainly. But here is the problem with the tax narrative: Argentina levies higher taxes than the United States on most income categories. It is not a tax haven. Residents pay progressive income tax of up to 35 percent on worldwide income, plus a wealth tax on global assets. If the goal were purely tax minimisation, Singapore or Dubai would have been the obvious answer.

So why Argentina? The answer is Javier Milei. Thiel has been publicly and enthusiastically aligned with Milei's libertarian project since before the 2023 election. He is not simply relocating to a country with a friendly leader. He is making a bet on a political experiment: a country choosing radical deregulation, the dismantling of an entrenched bureaucratic state, and an attempt to rebuild an economy from first principles. For someone whose entire intellectual identity is built on contrarian conviction and a belief that the prevailing consensus is usually wrong, this is enormously compelling. Add to that Thiel's publicly stated concerns about AI risk and the concentration of technology infrastructure in the Northern Hemisphere, Buenos Aires sits well outside those flashpoints, plus a world-class city where you can live extraordinarily well at low cost, and the decision makes complete sense on its own terms.

The broader pattern is worth noting. The ultra wealthy are asking harder questions than "where do I pay the least tax?" They are asking what they are moving toward: the values, the vision, the opportunity for the next generation, the world they want to help shape. Tax is a factor. It is rarely the whole answer.

Part Two: The Major Tax Jurisdictions

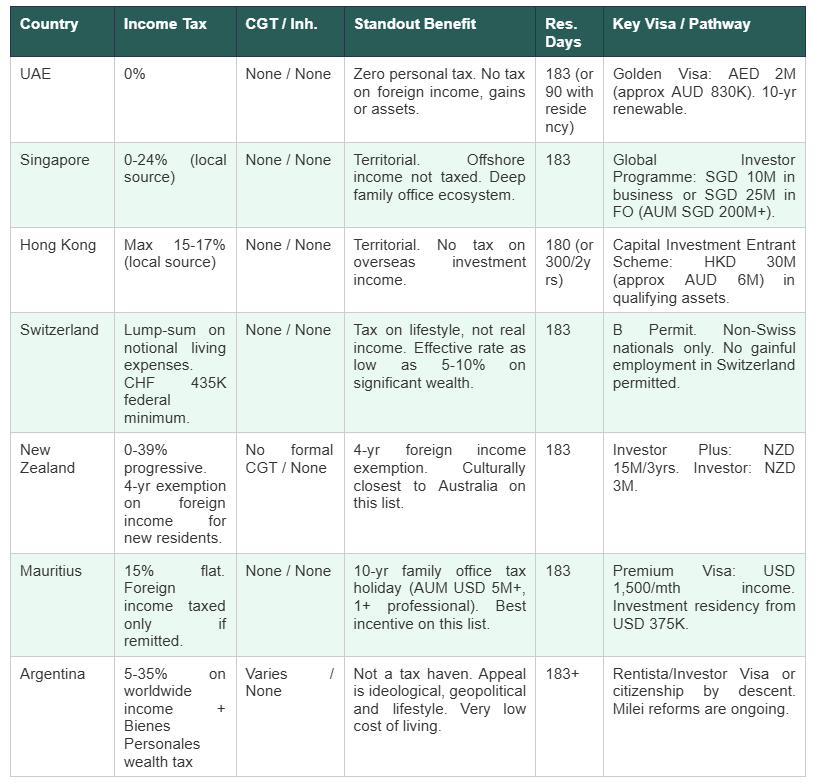

For those doing the analysis seriously, here is what the major jurisdictions actually offer. The table summarises the basics. The key points worth noting are below.

Tax rules are subject to change. This reflects the position as at June 2026 and is not tax or legal advice. Engage specialist advice in each jurisdiction before making any decisions.

The UAE leads on pure tax efficiency but requires genuine cultural adaptation and an analysis of geopolitical risk. Singapore is the most sophisticated option for family offices and has the governance depth that Australian families tend to value, but the entry bar is high. Hong Kong remains excellent on paper but the political shifts since 2019 cannot be separated from a long-term family decision. Switzerland's lump-sum regime is genuinely unique and can reduce effective rates dramatically, but it works best for people who want to actually live there, not park assets. New Zealand is the most underrated option for Australian families: culturally familiar, no capital gains tax and a four-year exemption on foreign income for new residents. Mauritius is the one to watch, particularly for family offices, with a 10-year tax holiday that nothing else on this list matches. Argentina is not a tax destination, it is a values destination.

Part Three: Structures, Not Just People

One of the most common misconceptions I encounter is that establishing a trust, company, or investment structure in a low-tax jurisdiction automatically reduces Australian tax exposure. It does not, at least not without significant additional steps.

The Australian rules that follow you

Australia's Controlled Foreign Company (CFC) rules mean that if an Australian tax resident controls a foreign company, the ATO can attribute that company's passive income (dividends, interest, royalties) directly back to the Australian resident and tax it here, whether or not a cent is distributed. Foreign trust rules work similarly: if an Australian resident established or transferred assets to a foreign trust, income can be attributed to them regardless of whether distributions are made.

The other critical rule is central management and control. A foreign company is treated as an Australian tax resident if its board effectively makes decisions from Australia. This catches a lot of structures set up offshore but run from Australia.

What happens when money comes back

If an offshore structure distributes income to an Australian resident, that distribution is generally taxable in Australia. If Australian residents use offshore funds to purchase Australian assets or to live in Australia, the ATO can treat that as income repatriated to Australia. The round-trip problem is real and the ATO watches for it carefully.

When offshore genuinely works

The scenario where offshore structures achieve meaningful tax reduction is when they are combined with genuine departure from Australia. A non-resident is only taxed in Australia on Australian-sourced income. If the controlling individuals are genuinely non-resident, the company or trust is genuinely managed from offshore, the income is genuinely foreign-sourced and the money is genuinely spent outside Australia, then yes, Australian tax can be avoided legitimately. Every one of those conditions needs to hold. The ATO applies the General Anti-Avoidance Provisions aggressively to structures where the substance does not match the form.

The practical implication: offshore structures are useful planning tools for families who are actually relocating. They offer very limited benefit for families who remain in Australia and are simply trying to move assets offshore on paper. A specialist tax adviser who understands both Australian law and the target jurisdiction is non-negotiable before any of this is considered seriously.

Part Four: Australia in Honest Comparison

Australia is genuinely exceptional. The healthcare system, education, natural environment, civic institutions and the culture are all world-class. I have lived overseas twice and came back both times. That should tell you something.

But the tax trajectory is concerning, particularly for entrepreneurs and business builders. The top marginal rate of 47 percent, the proposed minimum tax on discretionary trust distributions, a departure tax that crystallises CGT on unrealised gains the moment you leave and the ATO's increasingly sophisticated approach to offshore structures all point in the same direction. The policy settings are treating wealth as something to be constrained rather than something to be cultivated.

For most Australian families, staying makes sense. Life is too good and the roots too deep. But for those who are genuinely considering their options, the comparison is worth doing honestly: not just on tax rates, but on what kind of life you want to build, where your values are best expressed and what you are moving toward. Those are the questions the most thoughtful families are asking.

Georgia Barkell is the founder of Kinexis, a strategy, governance and operations consultancy for significant families.

This article is for informational purposes only and does not constitute legal, financial or tax advice. Readers should seek independent professional advice before making any decisions based on information contained in this article.